The State of Public Car Charging Part 1: the U.S.

The uneven growth and challenges of the US EV charging infrastructure.

Summary: The biggest design challenges right now seem to be making the experience more reliable, reducing friction between different networks, and building infrastructure that actually matches how people use EVs rather than how planners assume they will.

The public EV charging situation in the U.S. is growing quickly, but it still feels uneven and a bit unfinished. There are a lot more chargers than there were a few years ago, but where they are and how they work isn’t consistent yet.

One of the biggest things you notice is how uneven the distribution is. Chargers are heavily concentrated in cities and along the coasts, while rural areas still don’t have much coverage. That shows up in surveys too. About 44% of U.S. consumers say charging infrastructure in their area isn’t sufficient. At the same time, most EV charging actually happens at home or at work, not at public stations, so public chargers end up being more of a backup system than the main one.

The rollout has been pretty fast, just not fast enough to hit long-term goals. Around 35,000 public charging points were added in 2024. In 2025, more than 18,000 new fast-charging ports were installed, bringing the total number of fast chargers to over 70,000. Even with that growth, the U.S. would need to add about 58,000 chargers per year to stay on track for 2030 targets, so there’s still a gap.

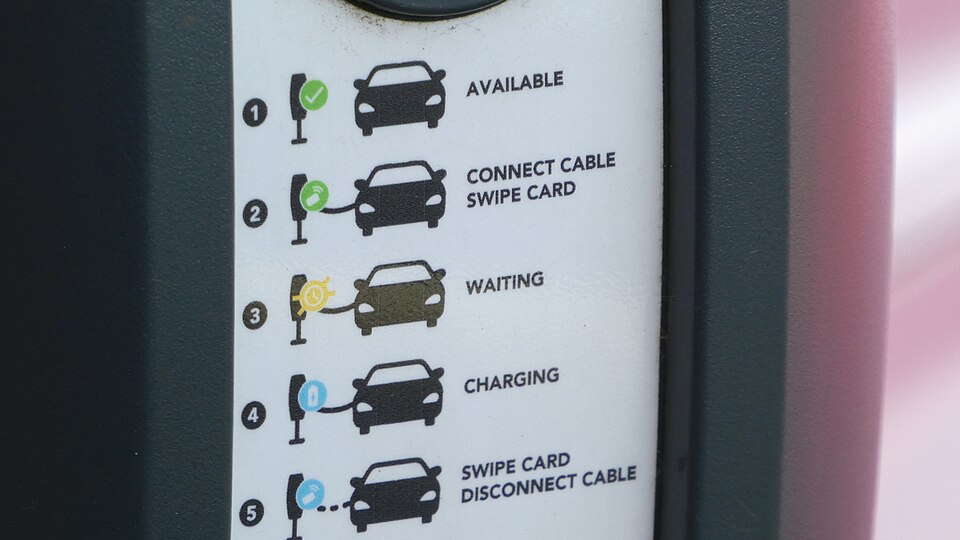

In terms of design, the hardware is starting to look pretty similar across companies. Most chargers follow the same general format, and the differences are less about how they look and more about how well they work. Reliability has been improving. Failed charging attempts are at their lowest level in four years, and about 80% of EV drivers say things have gotten better. So the experience is slowly becoming more predictable, which is probably more important than adding new features.

Ownership is kind of all over the place. Most chargers are run by private companies, sometimes in partnership with places like supermarkets, malls, or gas stations. Utilities are also involved, and governments mostly fund projects rather than run them. The federal NEVI program is a big example of that. It has $5 billion allocated and can cover up to 80% of project costs. But so far, it hasn’t made up a huge share of the actual network. In 2025, only about 3% of new fast chargers came from NEVI-funded projects, and fewer than 200 of those stations were operating as of 2024.

The business side is still figuring itself out. Most chargers now use a price-per-kilowatt-hour model, which makes up more than 80% of fast charging pricing. Prices are surprisingly similar across the country, usually somewhere between $0.45 and $0.53 per kWh, with most stations falling between $0.41 and $0.65. Some places are starting to vary prices by time of day, which can change costs by 50% to 100% depending on when you charge. That reflects how electricity pricing works behind the scenes, even though users don’t always see that complexity directly.

One thing that stands out is how much policy affects everything. The federal government is pushing infrastructure through funding programs like NEVI, but there have also been delays and uncertainty. Reviews and pauses in 2025 slowed things down and made planning harder for companies. On top of that, local permitting rules and utility pricing can vary a lot, which makes it harder to build chargers consistently across different regions.

There are also a few things about the system that are a bit counterintuitive. Even though public charging gets a lot of attention, it’s not what most people rely on day to day. Infrastructure has kept expanding even when EV sales slowed down, which suggests companies and governments are building ahead of demand. And pricing doesn’t vary as much as you might expect, so competition seems to be more about location and reliability than cost.